Over the Weekend President Trump fired Rohit Chopra the Director of the Consumer Finance Protection Bureau (CFPB) and today replaced him with Treasury Secretary (and hedge fund oligarch) Scott Bessent.

Over the Weekend President Trump fired Rohit Chopra the Director of the Consumer Finance Protection Bureau (CFPB) and today replaced him with Treasury Secretary (and hedge fund oligarch) Scott Bessent.

Within hours Bessent directed the Agency to halt all work on pending regulations and enforcement actions.

While many of our clients, friends, family and neighbors voted for President Trump, I’m pretty sure that their primary objective in supporting him was not to allow debt collectors, payday lenders, credit card companies, banks and mortgage companies to be given license to cheat them.

This is sad to watch because the CFPB has established itself as a strong independent regulator of financial services companies, mortgage companies, small business lenders, banks and non-bank lenders.

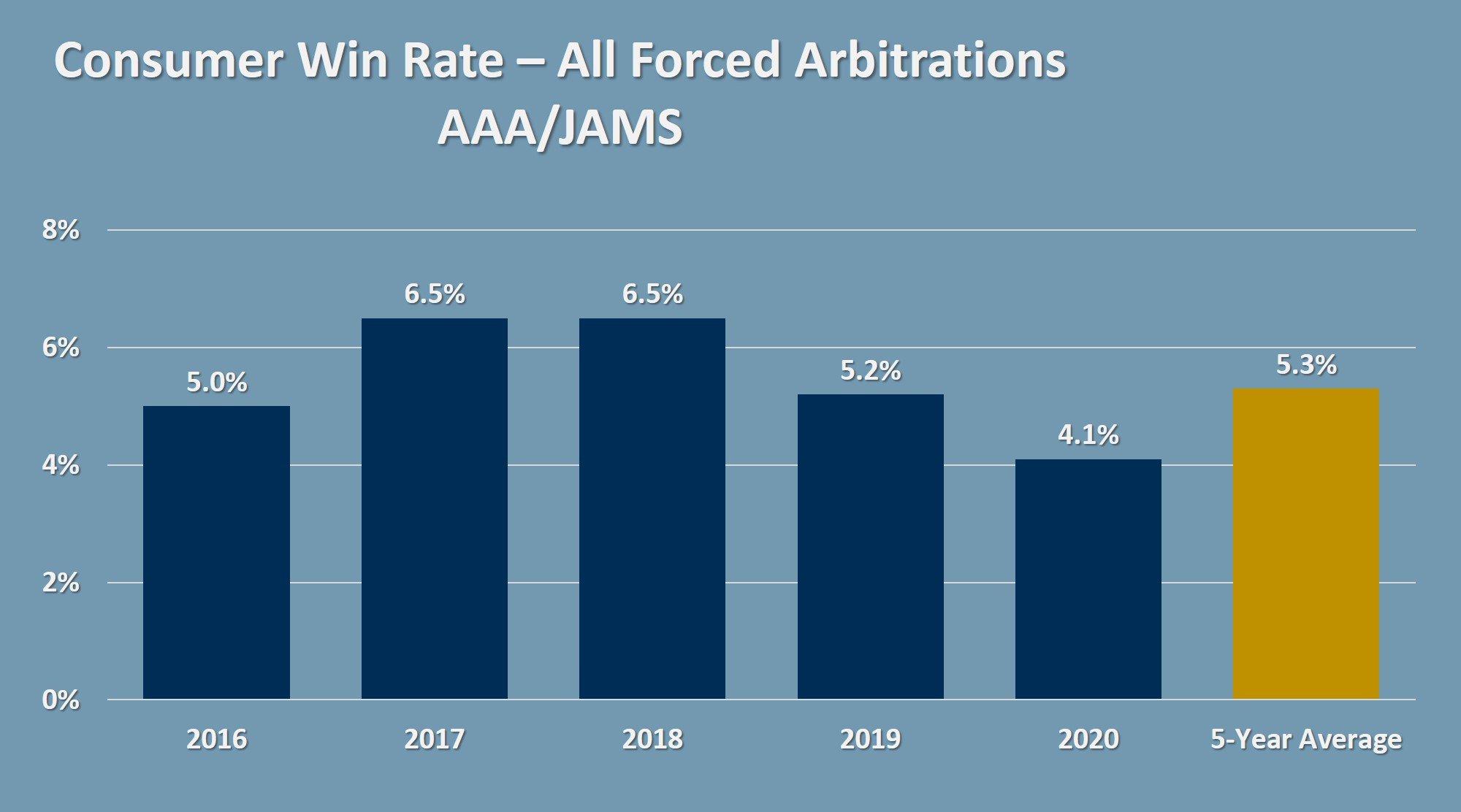

This is particularly important right now because most of the contracts offered by many of these financially predatory companies force their customers to private arbitration and prohibit participation in class action lawsuits against them. This means that if companies choose to cheat a little bit from a lot of people it’s even more difficult for private lawyers like those at DannLaw to hold them accountable in a meaningful way. If the CFPB is gone as a line of defense companies will have more license to cheat.

The consumers protected by the CFPB include all of us, even the CEOs and shareholders of the bad acting financial institutions. But it is critical to remember that the lack of accountability for bad actors in the financial services world also punishes ethical businesses who are trying to compete with the businesses that are cheating their customers. It’s often more expensive and less profitable to follow the law than to find ways to avoid doing so.

Actions to scale back the CFPB’s enforcement and rulemaking efforts are going to cost millions of consumers billions of dollars over the next four years and limit the remedies available to consumers who are wronged. This is not a political opinion. This is a fact.

Fortunately for homeowners and many of our clients, federal law still prohibits arbitration provisions in mortgage contracts. And for those who are subject to arbitration agreements we have been a leader among lawyers in using the arbitration process to protect our clients.

In light of this week’s news our Lawyers, Paralegals and support staff are committed to doubling down our efforts to use the courts and the law to hold financial predators accountable and seek justice for consumers who they victimize. Our job in protecting consumers is more important than ever and I know we are up to the challenge.

DannLaw provides representation to consumers in the following fields:

Data Breach Class Actions

Business Litigation

In reaction to their inexcusable inaction, DannLaw has formed a Forced Arbitration Practice Group led by attorneys Alisa Adams and Kurt Jones who have extensive experience pursuing and winning forced arbitration claims. Alissa, Kurt, and the Group’s talented paralegals are ready, willing, and more than able to take on banks, financial services firms, and any company that is using forced arbitration to prey upon, rip off, or exploit their customers.

In reaction to their inexcusable inaction, DannLaw has formed a Forced Arbitration Practice Group led by attorneys Alisa Adams and Kurt Jones who have extensive experience pursuing and winning forced arbitration claims. Alissa, Kurt, and the Group’s talented paralegals are ready, willing, and more than able to take on banks, financial services firms, and any company that is using forced arbitration to prey upon, rip off, or exploit their customers. It should come as no surprise to anyone that we have once again filed class action suits against Wells Fargo. Despite having paid more than

It should come as no surprise to anyone that we have once again filed class action suits against Wells Fargo. Despite having paid more than  Data breaches that enable cyberthieves to steal and misuse victims’ sensitive and confidential information is a growing problem in the U.S. That is why we are expanding our Data Privacy and Security Practice Group and working with the legal community to develop strategies that will ensure we can pursue and secure justice and just compensation for those put at risk when corporations, government agencies, and other entities fail to protect the personal data in their possession. As part of that effort, I am pleased to report that I was recently invited to serve on the prestigious

Data breaches that enable cyberthieves to steal and misuse victims’ sensitive and confidential information is a growing problem in the U.S. That is why we are expanding our Data Privacy and Security Practice Group and working with the legal community to develop strategies that will ensure we can pursue and secure justice and just compensation for those put at risk when corporations, government agencies, and other entities fail to protect the personal data in their possession. As part of that effort, I am pleased to report that I was recently invited to serve on the prestigious

Franklin County Common Pleas Court Judge Michael Holbrook ruled today that a class action lawsuit filed by DannLaw on behalf of Ohioans impacted by Governor Mike DeWine’s decision to terminate fully federally-funded Pandemic Unemployment Assistance (PUA) off payments in May of 2021 may continue. In a 16-page order Judge Holbrook denied Attorney General Dave Yost’s motion to dismiss the suit and said the plaintiffs had “…sufficiently plead claims for declaratory judgment, injunctive relief, and petitions for writs of mandamus. He also scheduled a status conference for Tuesday, April 9, 2024, at 1:30 PM. Judge Holbrook’s order may be viewed here:

Franklin County Common Pleas Court Judge Michael Holbrook ruled today that a class action lawsuit filed by DannLaw on behalf of Ohioans impacted by Governor Mike DeWine’s decision to terminate fully federally-funded Pandemic Unemployment Assistance (PUA) off payments in May of 2021 may continue. In a 16-page order Judge Holbrook denied Attorney General Dave Yost’s motion to dismiss the suit and said the plaintiffs had “…sufficiently plead claims for declaratory judgment, injunctive relief, and petitions for writs of mandamus. He also scheduled a status conference for Tuesday, April 9, 2024, at 1:30 PM. Judge Holbrook’s order may be viewed here:  I appreciate everyone’s patience with the slow progress of our case seeking payment of the Pandemic Unemployment Supplemental Benefits that were denied to Ohioans by Governor DeWine and the Ohio Department of Jobs and Family Services. As an FYI, I emailed Judge Holbrook’s law clerk

I appreciate everyone’s patience with the slow progress of our case seeking payment of the Pandemic Unemployment Supplemental Benefits that were denied to Ohioans by Governor DeWine and the Ohio Department of Jobs and Family Services. As an FYI, I emailed Judge Holbrook’s law clerk