We love receiving shout-outs from our clients—even from those who took a little while to become our clients.

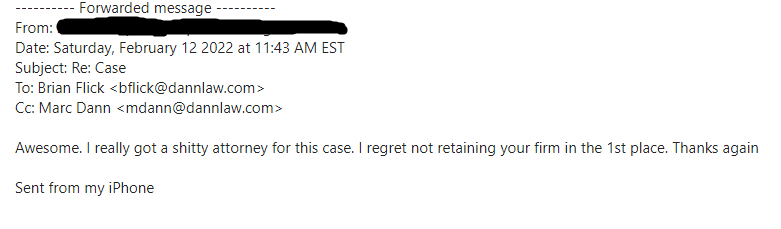

We love receiving shout-outs from our clients—even from those who took a little while to become our clients.WE Just received this email from a person who contacted us in November of 2021because he was not happy with the lawyer who was handling his bankruptcy. He spoke to Brian Flick, leader of DannLaw’s Bankruptcy Practice Group at the time, but decided to stick with the law firm he had hired.

He reached out to us again three months later and asked if we could help him save his home.

Our answer: absolutely.

His response was priceless.

If you are facing foreclosure, need to negotiate a loan modification, or are attempting emerge from mortgage forbearance, don’t delay, schedule a no-cost, no-obligation consultation today.

You can contact us by phone at (216) 373-0539, DM us via the DannLaw Facebook page, or complete and submit our contact form: https://dannlaw.com/contact/

As this client learned, we will always be here to help…Read the entire email string below.

From: xxxx

From: xxxx

Date: Saturday, February 12 2022 at 11:43 AM EST

Subject: Re: Case

To: Brian Flick <bflick@dannlaw.com>

Cc: Marc Dann <mdann@dannlaw.com>,

Awesome. I really got a shitty attorney for this case. I regret not retaining your firm in the 1st place. Thanks again

Sent from my iPhone

On Feb 12, 2022, at 10:37 AM, Brian Flick <bflick@dannlaw.com> wrote:

xxxx,

Good to hear from you.

Can you check my calendar for Tuesday, Wednesday or Thursday via Calendly to find a time that works for you based on my availability?

Thank you.

Brian D. Flick, Esq.

DannLaw

On Fri, Feb 11, 2022 at 7:24 PM xxxx wrote:

Hi Brian

I spoke with you before about my chapter 13 case. It was dismissed. I would like to try and work with first and second mortgage companies to keep my house. My phone number is 14404129455

Thanks

xxxx

Sent from my iPhone

On Nov 22, 2021, at 5:42 PM, Brian Flick <bflick@dannlaw.com> wrote:

Sounds good.

Brian D. Flick, Esq.

DannLaw

On Mon, Nov 22, 2021 at 5:30 PM xxxx wrote:

I’ll ring you up wends at 10

Sent from my iPhone

On Nov 22, 2021, at 4:53 PM, Brian Flick <bflick@dannlaw.com> wrote:

xxxx,

I have some availability tomorrow and Wednesday. Best window would be Wednesday before 11.

Thank you.

Brian D. Flick, Esq.

DannLaw

On Mon, Nov 22, 2021 at 4:51 PM xxxx wrote:

Brian

I did not want to be a jerk and call you on a Friday night. Just let me know what works and I’ll be available.

Thanks

xxxx

Sent from my iPhone

On Nov 19, 2021, at 4:37 AM, Brian Flick <bflick@dannlaw.com> wrote:

xxxx,

If you’d like to call me after 5, I can be available. I’m booked pretty solid all day until then.

Brian D. Flick, Esq.

DannLaw

On Nov 18, 2021, at 8:47 PM, xxxx wrote:

Brian

Sorry today turned into a wreck. If you can chat tomorrow it would be much appreciated. I’m very frustrated at how my case is being handled.

Thanks

xxxx

Sent from my iPhone

On Nov 18, 2021, at 10:39 AM, Brian Flick <bflick@dannlaw.com> wrote:

xxxx,

Feel free to call me at your convenience today. I’ve got a quick call at 11, 12, am out for a personal matter from 1:30-3ish and then quick calls at 4 and 4:30.

Thank you.

Brian D. Flick, Esq.

DannLaw

On Thu, Nov 18, 2021 at 9:25 AM xxxx wrote:

Sounds great. Anytime today or tomorrow is cool. Just let me know

Sent from my iPhone

On Nov 16, 2021, at 6:01 PM, Brian Flick <bflick@dannlaw.com> wrote:

How about Thursday at 10:30?

Brian D. Flick, Esq.

DannLaw

On Tue, Nov 16, 2021 at 5:31 PM xxxx wrote:

Thank you for the quick response. I have a call with chapter 13 trustee on 930 am on Thursday, so anytime after that. I’m also available on Friday as well

Thanks

xxxx

Sent from my iPhone

On Nov 16, 2021, at 12:44 PM, Brian Flick <bflick@dannlaw.com> wrote:

xxxx:

Marc forwarded your email to me as I manage the firm’s bankruptcy practice.

I have reviewed the docket for your case and we’d be happy to discuss representation. What is your availability on Thursday or Friday for an extended call?

Thank you.

Brian D. Flick, Esq.

DannLaw

From: xxxx

Date: Tuesday, November 16 2021 at 11:01 AM EST

Subject: Case

To: Marc Dann <mdann@dannlaw.com>

Hello sir

I have filed bankruptcy but I’m having issues with my current representation. If I can’t get any help that we discussed previously, is it possible we could chat and maybe have you take over this case?

Thanks

xxxx

Sent from my iPhone

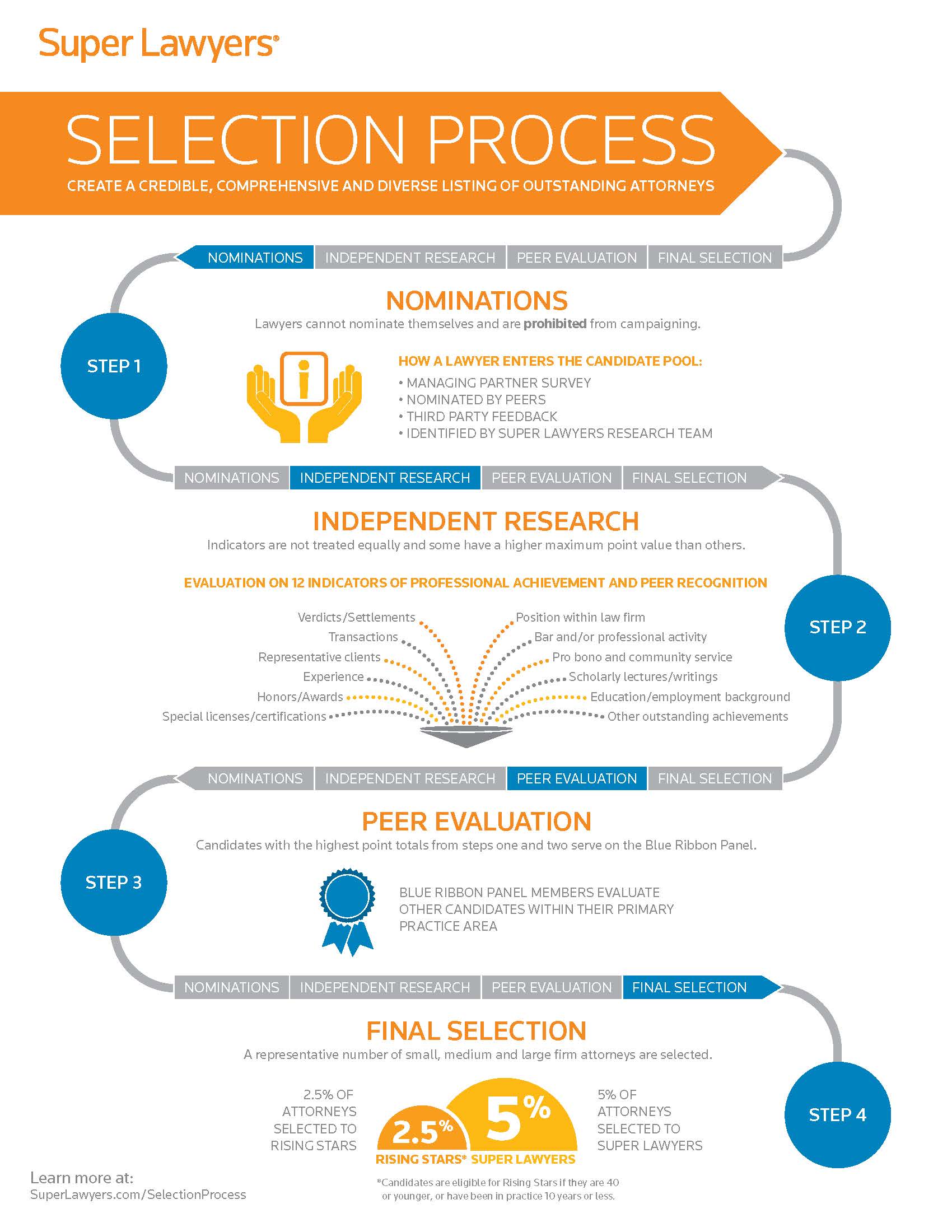

One of America’s most prestigious attorney rating services has just confirmed what his colleagues at DannLaw and the thousands of clients he has represented have long known: Brian Flick is a “SuperLawyer” in the field of consumer law. Super Lawyers selects attorneys using a patented multi-phase process that combines peer nominations and evaluations with independent research. Each candidate is evaluated on 12 indicators of professional achievement. Those who score highest then undergo a “blue ribbon” peer review by practice area. Only the highest-rated attorneys make the Super Lawyer list for each state and the designation is reserved for attorneys who excel in their field, contribute to their community, and abide by the highest professional and ethical standards. We are extremely proud that Brian is listed among them.

One of America’s most prestigious attorney rating services has just confirmed what his colleagues at DannLaw and the thousands of clients he has represented have long known: Brian Flick is a “SuperLawyer” in the field of consumer law. Super Lawyers selects attorneys using a patented multi-phase process that combines peer nominations and evaluations with independent research. Each candidate is evaluated on 12 indicators of professional achievement. Those who score highest then undergo a “blue ribbon” peer review by practice area. Only the highest-rated attorneys make the Super Lawyer list for each state and the designation is reserved for attorneys who excel in their field, contribute to their community, and abide by the highest professional and ethical standards. We are extremely proud that Brian is listed among them.

Founder Marc Dann and Managing Partners Brian Flick and Javier Merino are pleased to announce that DannLaw has acquired the Zingarelli Law Office, one of the Cincinnati area’s most highly respected consumer and small business bankruptcy law firms.

Founder Marc Dann and Managing Partners Brian Flick and Javier Merino are pleased to announce that DannLaw has acquired the Zingarelli Law Office, one of the Cincinnati area’s most highly respected consumer and small business bankruptcy law firms.

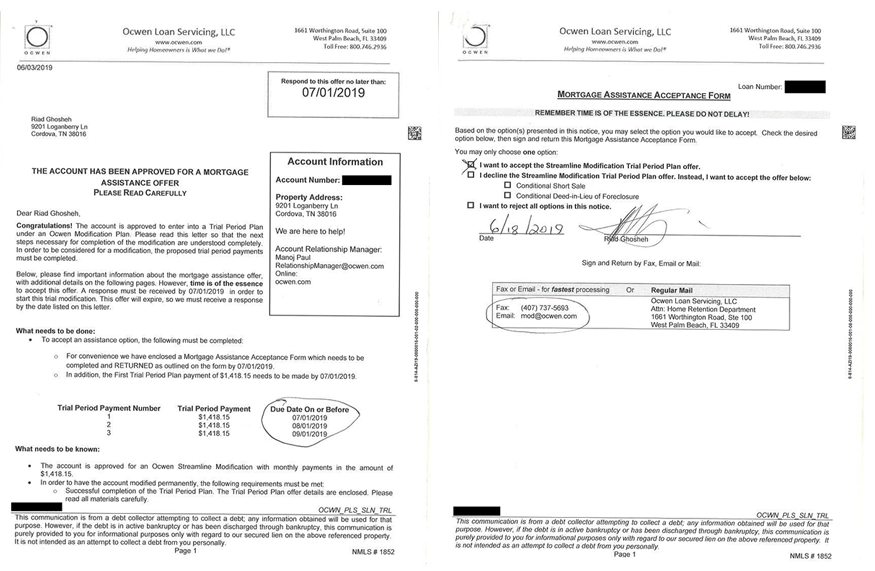

A recent federal appeals court decision may spell “relief” for Americans buried under private student loan debt held by Navient. In a unanimous decision, a three-judge panel of the Court of Appeals for the Fifth Circuit held that Navient private student loans ARE dischargeable in bankruptcy.

A recent federal appeals court decision may spell “relief” for Americans buried under private student loan debt held by Navient. In a unanimous decision, a three-judge panel of the Court of Appeals for the Fifth Circuit held that Navient private student loans ARE dischargeable in bankruptcy.