I am pleased to announce that attorneys Kurt Jones, Alisa Adams and Andy Engel as well as paralegals Maureen Dial, Madellyn Brown, and Ivona Gates who were formerly associated with Advocate Attorneys LLP have joined DannLaw and will now represent their consumer arbitration clients as members of our outstanding legal team.

The seamless transition of the Advocate staff to DannLaw will ensure that clients continue to work with the attorneys and support staff they know and trust and that cases will proceed without undue disruption or delay.

We welcome our new colleagues, and we look forward to providing their clients with exceptional level of professional service that has made DannLaw one of the nation’s leading consumer protection and class action litigation law firms.

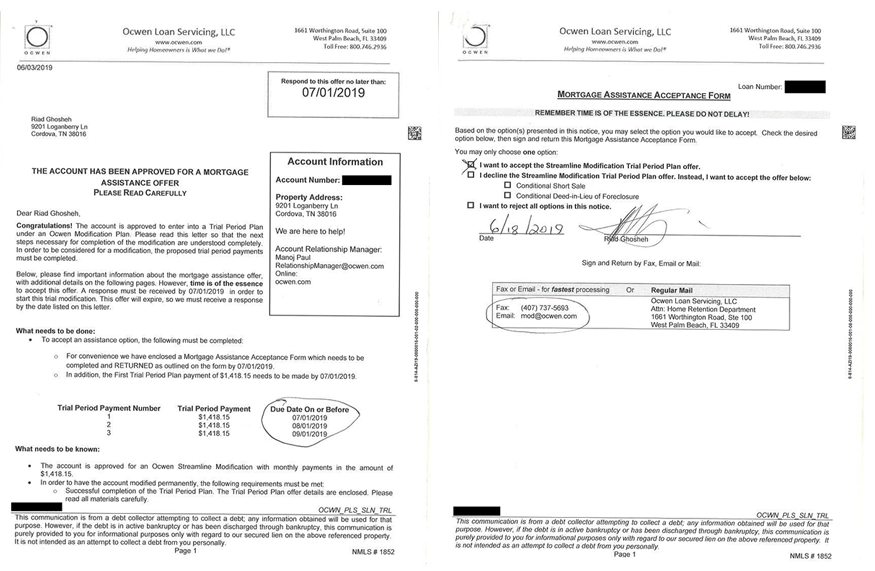

Along with forbearance and other relief programs, foreclosure stays are ending. That means hundreds and perhaps thousands of new judicial foreclosure actions will be filed in Ohio, New Jersey and other states. We have the experience, expertise, and knowledge needed to save your home.

Along with forbearance and other relief programs, foreclosure stays are ending. That means hundreds and perhaps thousands of new judicial foreclosure actions will be filed in Ohio, New Jersey and other states. We have the experience, expertise, and knowledge needed to save your home. Multiple courts have selected DannLaw to serve as Class Counsel in data breach Cases. A data breach occurs when a company fails to properly safeguard its customers’ personal information. Our legal staff devotes considerable time and resources to pursuing and securing just compensation for the inconvenience, expense, and aggravation data breach victims endure.

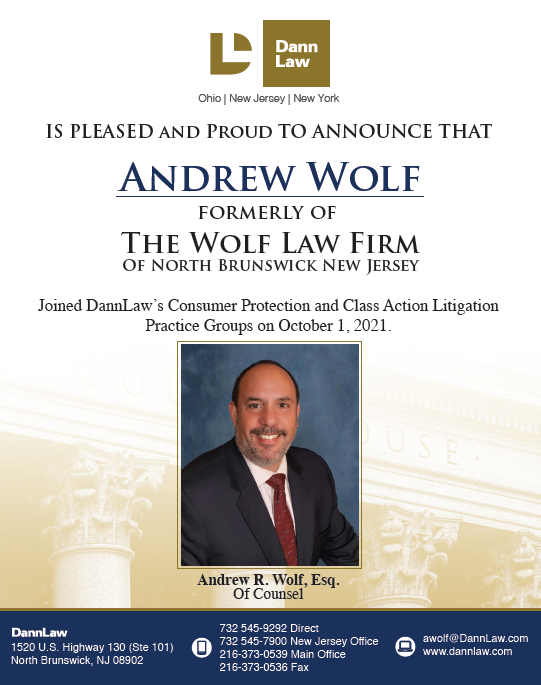

Multiple courts have selected DannLaw to serve as Class Counsel in data breach Cases. A data breach occurs when a company fails to properly safeguard its customers’ personal information. Our legal staff devotes considerable time and resources to pursuing and securing just compensation for the inconvenience, expense, and aggravation data breach victims endure. DannLaw founder and former Ohio Attorney General Marc Dann announced today that Attorney Andrew Wolf of North Brunswick, New Jersey has become an “Of Counsel” member of DannLaw’s Consumer Protection and Class Action Litigation Practice groups. Wolf, who has earned a reputation as one of the nation’s most effective consumer advocates will be based in DannLaw’s New Jersey/New York office.

DannLaw founder and former Ohio Attorney General Marc Dann announced today that Attorney Andrew Wolf of North Brunswick, New Jersey has become an “Of Counsel” member of DannLaw’s Consumer Protection and Class Action Litigation Practice groups. Wolf, who has earned a reputation as one of the nation’s most effective consumer advocates will be based in DannLaw’s New Jersey/New York office. If you are a former Home Savings or First Federal customer who now banks with Premier, contact us TODAY so we can protect your family’s financial future and fight for the monetary compensation you need and deserve.

If you are a former Home Savings or First Federal customer who now banks with Premier, contact us TODAY so we can protect your family’s financial future and fight for the monetary compensation you need and deserve.

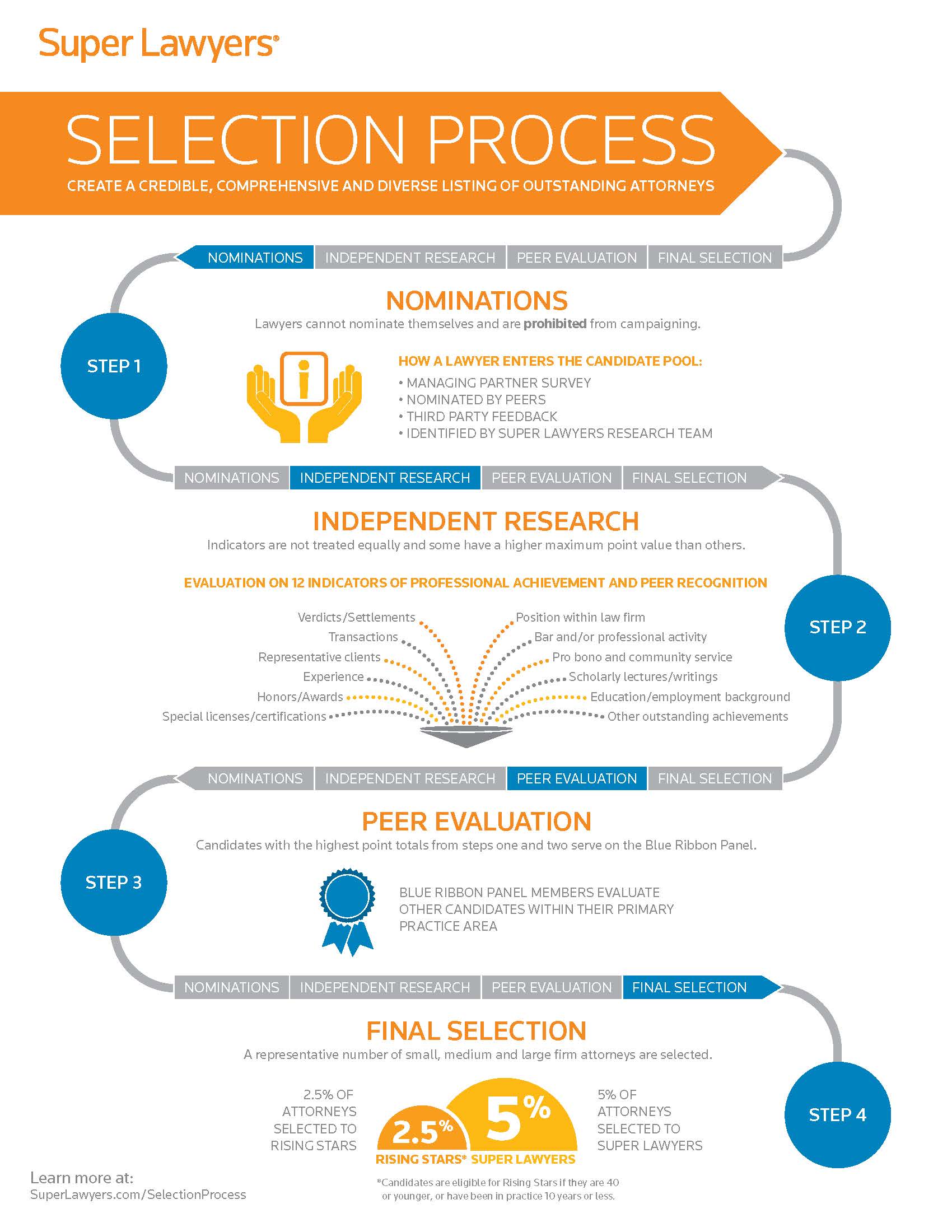

One of America’s most prestigious attorney rating services has just confirmed what his colleagues at DannLaw and the thousands of clients he has represented have long known: Brian Flick is a “SuperLawyer” in the field of consumer law. Super Lawyers selects attorneys using a patented multi-phase process that combines peer nominations and evaluations with independent research. Each candidate is evaluated on 12 indicators of professional achievement. Those who score highest then undergo a “blue ribbon” peer review by practice area. Only the highest-rated attorneys make the Super Lawyer list for each state and the designation is reserved for attorneys who excel in their field, contribute to their community, and abide by the highest professional and ethical standards. We are extremely proud that Brian is listed among them.

One of America’s most prestigious attorney rating services has just confirmed what his colleagues at DannLaw and the thousands of clients he has represented have long known: Brian Flick is a “SuperLawyer” in the field of consumer law. Super Lawyers selects attorneys using a patented multi-phase process that combines peer nominations and evaluations with independent research. Each candidate is evaluated on 12 indicators of professional achievement. Those who score highest then undergo a “blue ribbon” peer review by practice area. Only the highest-rated attorneys make the Super Lawyer list for each state and the designation is reserved for attorneys who excel in their field, contribute to their community, and abide by the highest professional and ethical standards. We are extremely proud that Brian is listed among them.